By David J. Gibson, MD

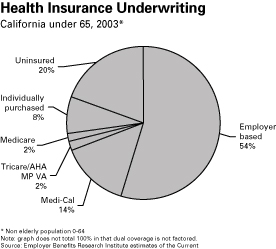

THE CONCEPT OF A STATE-BASED HEALTH care system seems to recycle every few years, as the inadequacies of the current employer-based financing system become more apparent. The arguments for using the government to enforce the pooling of risk across the entire population make eminent sense from a purely actuarial perspective. The graph on the next page shows the sources for health care underwriting in California today.However, whenever such a system is presented to the voters, it does not fly. For example, in 1994, Californians resoundingly defeated Proposition 186, a single-payer health-care initiative. In November of 2002, Oregon voters defeated a measure that would have provided universal health care for state residents. It failed by almost a 4 to 1 margin. Last year California voters rejected Proposition 72, a referendum to support SB 2, which was a state law requiring employers to provide health care benefits to workers. It is of interest that despite intensive support by unions, the California Medical Association and a host of consumer groups, the proposition went down to defeat.

So, why do voters instinctively react negatively to a concept that is inherently sound? Why do they consistently reject pooling of health care risk by the government when the evidence that the fractured employer-based risk pool structure is collapsing? Here is the answer. Americans have lost confidence in the competency of their political system.

Politicians at all levels of government have demonstrated that they lack the self discipline required to competently govern. Thus, these politicians cannot be trusted with America's health care system. You do not get re-elected by saying no to special interests, even when their demands represent bad public policy.

The support for this assertion can be found here in California. The state's economy generates $1.3 trillion in annual output and is the fifth or sixth largest economy in the world. During the dot com bubble in the mid to late 1990s, California politicians, responding to entrenched special interests, created a structural budget deficit of such magnitude that even if the state fired every single person on the payroll - every park ranger, every college professor and every Highway Patrol officer - it would still be more than $6 billion short. No public or private company in America could survive with this quality of leadership. Self-disciplined politicians is an oxymoron.

State governments regulate health insurance companies. In the past, state legislatures have not resisted the demands of politically active special interest groups when it comes to mandating health insurance benefits. These mandates require insurers to cover specific services and specific providers. Currently, there are 1,823 state-mandated benefits among the 50 states, and an additional 295 mandates are now being debated in state legislatures.ą

Mandates cover services ranging from acupuncture to in vitro fertilization. They cover providers ranging from chiropractors to naturopaths. They cover bone marrow transplants in New Jersey, hairpieces for chemotherapy patients in Minnesota, marriage counseling in Connecticut and pastoral counseling in Maine.

The accompanying table summarizes the data in which: 11 states require insurers to cover marriage counselors, 4 mandate coverage for naturopaths, 3 cover midwives, 11 cover acupuncturists and 4 require coverage for massage therapists. Other states have mandated such procedures as in vitro fertilization (15 states), port-wine stain birthmark removal (2 states), and treatments for morbid obesity (4 states).

These laws mean that if people buy insurance at all, they must purchase an unnecessarily expensive package of benefits designed by politicians. They are not offered an option to buy insurance that reflects their own preferences, tailored to individual and family needs.

This political tinkering with the scope of health care benefits results in disastrous public policy outcomes. Compared to the costs of barebones insurance, these kinds of mandated benefits hike premiums considerably and price otherwise healthy people out of the market. It is now estimated that one of every four uninsured Americans has been priced out of the health insurance market by these politically derived mandates. As a result, risk pools shrink and existing health insurance products become progressively expensive with unsustainable cost trends.

If mandates do so much harm, then why do they exist? The record demonstrates that very few mandates have been enacted because of patient pressure. Most are the result of the lobbying power of special interest service vendors. And once a state-mandated health benefit is enacted, it is almost impossible to get it repealed.

It is an inescapable reality that private health care funding is failing. There is a clear need to pool the health risk across the entire population or insurance underwriting will not survive. Unfortunately, with good reason, Americans lack confidence in the competence of the political process to govern competently. Thus a lack of political credibility is standing in the way of a common sense and readily achievable solution to the growing health care financing problem in this country.

|

|

© David J. Gibson, MD 2007